|

This is the first post in a series highlighting the top five reasons why people file bankruptcy. The March 2017 annual bankruptcy filings totaled 794,492, compared with 833,515 cases in the year ending March 2016. While there are a number of reasons why Americans file for bankruptcy, the reasons for filing can be grouped into five major categories. The fifth most common reason is unexpected expenses. Loss of property due to theft or casualty, such as earthquakes, floods or tornadoes for which the owner is not insured can force some into bankruptcy. Others may be faced with substantial car repairs or other major catastrophes which can quickly drain your bank account.

If you are considering bankruptcy as an option to address unexpected expenses, contact a Bankruptcy Attorney at 636-724-3355 or visit www.bankruptcysolo.com to schedule your no-cost consultation with a bankruptcy attorney.  There are many myths surrounding personal bankruptcy. Here’s a look at some of the most common myths. Myth 1: Bankruptcy is Because of Financial Irresponsibility. Yes there are situations where this is the case. However, many people file bankruptcy due to circumstances that are outside their control. For instance, many bankruptcies are due to medical bills linked to unforeseen health issues. Other common reasons include loss of a job or divorce. Myth 2: Bankruptcy Permanently Ruins Your Credit. Filing bankruptcy will impact your credit upon filing, however, after a year of filing bankruptcy most debtors find their credit scores have increased on average 125 points from the date of filing. Myth 3: Bankruptcy Discharges all Past Debts. Unfortunately no. There are several types of debt that are not discharged by bankruptcy. Domestic support obligations such as alimony or child support cannot be discharged through bankruptcy. This also applies to restitution related to a prior crime and the vast majority of overdue taxes. Myth 4: You Can’t File Bankruptcy if You have a Job. This is not true. Many people who are currently employed are able to qualify for bankruptcy if their income falls below a minimum threshold. Myth 5: You’ll Lose Everything. Filing for bankruptcy does not necessarily mean that you will lose all of your possessions. For the average person, most personal possessions are covered by exemptions. Call today at 636-734-3355 to talk to an attorney and determine if you qualify for bankruptcy.  If you file a Chapter 7 bankruptcy in Missouri, you can protect some or all of your property with Missouri’s bankruptcy exemptions. Here are 9 of the most common exemptions. 1. Homestead or Residential Property: The homestead exemption protects equity in your home. In Missouri, you can exempt a portion of the equity in the real estate in which you live or will live, or a portion of the equity in a mobile home in which you live (Mo. Rev. Stat. §513-430, 475) 2. Domestic Support: Including child support or alimony (Mo. Rev. Stat. §513.430) 3.Insurance Benefits: Life insurance dividends (Mo. Rev. Stat. §513.430), disability or illness benefits (Mo. Rev. Stat. §513.430), stipulated insurance premiums (Mo. Rev. Stat. §377.330), unmatured life insurance policy (Mo. Rev. Stat. §513.430) and assessment plan or life insurance proceeds (Mo. Rev. Stat. §377.090) 4. Motor Vehicle: Partial equity in motor vehicles (Mo. Rev. Stat. §513.430) 5. Personal Property: Partial value of furniture, clothing, books, appliances, animals, and instruments (Mo. Rev. Stat. §513.430), partial value in a wedding ring and other jewelry (Mo. Rev. Stat. §513.430) and health savings accounts (Mo. Rev. Stat. §513.040 ) 6. Life Insurance Benefits: Including, but not limited to, teachers’ retirement benefits (Mo. Rev. Stat. §169.090), ERISA-qualified benefits necessary for support (Mo. Rev. Stat. §513.430), firefighters’ retirement benefits (Mo. Rev. Stat. §§87.090, 87.365, 87.485), police department employees’ retirement benefits (Mo. Rev. Stat. §§87.190, 87.353, 86.1430) and public officers and employees’ retirement benefits (Mo. Rev. Stat. §§70.695, 70.755) 7. Public Benefits: Including, but not limited to, veterans’ benefits (Mo. Rev. Stat. §513.430), workers’ compensation (Mo. Rev. Stat. §287.260), unemployment compensation (Mo. Rev. Stat. §§288,380, 513.430), Social Security benefits, (Mo. Rev. Stat. §513.430) and public assistance, including earned income tax credit but not child tax credit (Mo. Rev. Stat. §513.430) 8. Tools of the Trade: Partial value of tools, implements, and books of your trade or business (Mo. Rev. Stat. §513.430) 9. Wildcard: Up to $1,200 in value of any property (Mo. Rev. Stat. §513.430) Missouri’s exemption amounts are adjusted periodically. To ensure that you have the most recent figures, be sure to consult with your bankruptcy attorney. Considering Bankruptcy? Work with an Attorney You can Trust. Schedule your free consultation by calling us at (636) 724-3355.  What you do, or don't do, prior to bankruptcy can have a big impact on the success of your bankruptcy. The actions you take prior to filing for bankruptcy can have a potentially irreversible impact on your bankruptcy filing. Here are 7 things to avoid before filing bankruptcy.

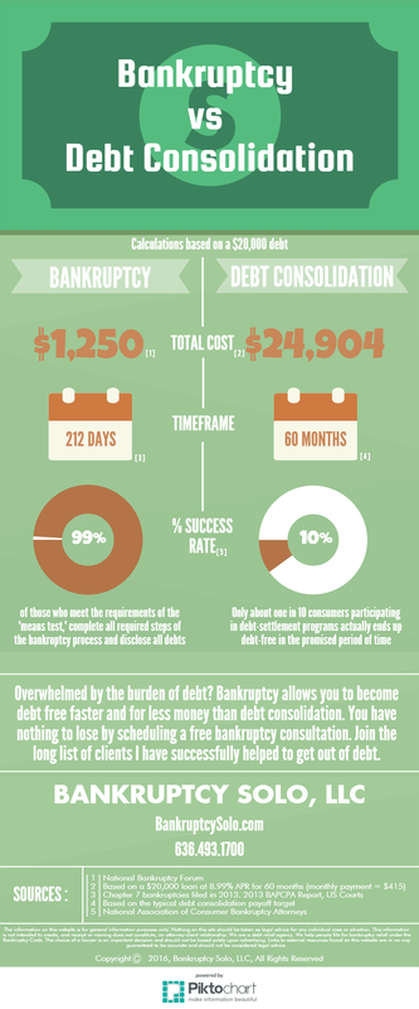

1. Provide Inaccurate, Incomplete or Dishonest Information You are required to provide complete and accurate information about all of your assets, debts, income, expenses and financial history. You do so under penalty of perjury. If you knowingly misrepresent your information, such as fail to disclose an asset, you could be subject to criminal prosecution. 2. Rack Up New Debt If you used a credit card to buy a luxury item within 90 days of filing bankruptcy, in an amount exceeding $600, than you may similarly be denied a discharge of that debt. Again, the creditor may file an objection to discharge of that debt, claiming you had no intention to repay it. 3. Move Assets Don't be tempted to sell, transfer for safekeeping, or hide assets before filing bankruptcy. If you do, you might be denied a discharge and even be subject to criminal penalties. 4. Favor One Creditor Over Another If you pay back loans to friends or relatives (within one year of filing), or even other creditors (within 90 days), then this may be considered a “preferential transfer.” The bankruptcy trustee may file an adversarial proceeding to get the money back from the person or entity you paid, and then disburse the money in equal shares across all of your creditors. 5. Fail to File Income Tax Returns Tax returns are crucial to determining your current and past earnings and asset holdings, as well as satisfying potential priority tax claims. 6. Ignore Impending Collection Actions Advise creditors right away of your intention to file bankruptcy. Your attorney may be able to stop attempts to take your property. Without filing there is no protection from creditors. 7. File When You are About to Receive Substantial Assets You should reconsider filing bankruptcy if you are about to receive an inheritance (within one year), a significant income tax refund, a settlement from a lawsuit, or repayment from a loan you made to someone else. In summary, filing for bankruptcy is a complex matter that should not be taken lightly. An attorney can help you to avoid these common mistakes and ultimately help you to get a fresh start. Call a Bankruptcy Attorney at 636-724-3355 or visit www.bankruptcysolo.com to discuss these and other complex legal matters at your free consultation.  Overwhelmed by the burden of debt? Bankruptcy allows you to become debt free faster and for less money than debt consolidation. You have nothing to lose by scheduling a free bankruptcy consultation. Join the long list of clients we have successfully helped to get out of debt.

www.BankruptcySolo.com 636-724-3355 In exchange for having your debts discharged or wiped out, an individual or couple filing for bankruptcy is required by law to disclose all of their assets in their petition. It is important for filers to remember that they must be 100 percent truthful when disclosing assets and not attempt to hide them. Some people think that by concealing assets, they won’t be taken away by the court during bankruptcy. However, doing so is considered perjury, which comes with a number of penalties which ultimately may end up costing the filer even more.

There are many reasons why an asset may go undisclosed by a filer. These include:

Bankruptcy trustees are very keen detectives and are not often fooled by hidden assets. All it takes is a public records review, a debt review, a review of bank records or tax returns, or a look at online asset searches to determine whether or not an asset has been hidden or transferred. If a filer is found to have attempted to conceal assets, they face a number of repercussions. Not only will their hidden assets not be eligible for discharge (meaning they will still owe the debt they were trying to get rid of with bankruptcy), but they may also get their discharge revoked. Worse still, they may face criminal penalties for perjury, which is punishable by up to five years in prison and/or a fine of up to $500,000. The following are examples of assets that are most commonly forgotten in bankruptcy petitions:

What happens if you make an honest mistake? Sometimes, though, assets are not disclosed simply because a person made a mistake without malicious intent. If this happens, the filer should immediately disclose the asset with their trustee. As long as the mistake was not made in an attempt to delay, hinder, or defraud creditors, the error should not result in a denial of a discharge. Considering Bankruptcy? Work With an Attorney You Can Trust If you are considering bankruptcy in the St. Charles / St. Louis area, please get in touch with me. I am prepared to assist you in taking your first step to a fresh start. Schedule your free consultation by visiting www.BankruptcySolo.com or by calling us at (636) 724-3355. When you file for bankruptcy, the “automatic stay” is put into place which effectively stopping creditors in their tracks. This is a United States bankruptcy code law that does not allow creditors or debt collection agencies to take action or file lawsuits against debtors. Not only can the automatic stay protect you against lawsuits regarding the debt that you owe, but it can also shield you from any further collection efforts by creditors, collection agencies, or government entities. In most cases, its reach will extend to foreclosures, auto repossessions, wage garnishments, and debt collections, making it a powerful tool for debtors.

With an automatic stay in place, creditors are prohibited from:

What if a Creditor Violates the Automatic Stay? If a creditor violates the automatic stay by continuing their collection efforts, attempting to seize your property, or garnishing your wages, they can be penalized by the court. Anyone who willfully violates the stay in your bankruptcy case can be held liable for actual damages caused by the violation and, in some cases, even punitive damages. How Long Will the Automatic Stay Protect Me? Generally, the automatic stay will remain in effect for the duration of your bankruptcy case. This means that, as long as you are involved in the bankruptcy process, creditors cannot take action against you. However, this also means that the automatic stay will be lifted once you have received a discharge and your bankruptcy case is closed. How Creditors Can Get Around the Automatic Stay Usually, a creditor can get around the automatic stay by asking the bankruptcy court to remove ("lift") the stay, if it is not serving its intended purpose. For example, say you file for bankruptcy the day before your house is to be sold in foreclosure. You have no equity in the house, you can't pay your mortgage arrears, and you have no way of keeping the property. The foreclosing creditor is apt to go to court soon after you file for bankruptcy and ask for permission to proceed with the foreclosure -- and that permission is likely to be granted. Call The Wibbenmeyer Law Firm, LLC for More Information Stop credit harassment today! Contact a Bankruptcy Attorney at 636-724-3355 or visit www.bankruptcysolo.com to schedule a free consultation with a bankruptcy attorney and find out if you are eligible for bankruptcy. Call today to take your first step to a fresh start! Bankruptcy is not an indicator of financial failure. In fact, according to the Institute for Financial Literacy, frequent causes of financial distress, which ultimately leader to bankruptcy, include unexpected expenses (56 percent), reduction in income (65 percent), job loss (43 percent) and illness/injury (31 percent). You should not feel ashamed about your financial situation, nor should bankruptcy be viewed as an admission of failure. For many, bankruptcy is the most appropriate option for achieving relief from overwhelming debt. Contact The Wibbenmeyer Law Firm, LLC today to schedule a free, no-risk consultation to understand your options and determine if you qualify for a bankruptcy. Take your first step to a fresh start. The Wibbenmeyer Law Firm, LLC is conveniently located in St. Charles, Missouri. 636-724-3355 / www.bankruptcysolo.com.

Debt consolidation it not an option to take lightly. Most do not know that it could end up costing you money in hidden fees and tax liability. More importantly, it could cost you your home or other valuable property.

You could lose your property. If you use property such as your home or vehicle as collateral for the debt consolidation loan, you could lose that property if you default on the loan payments. Beware of hidden costs. Although lower interest rates and monthly payments are appealing, a debt consolidation loan could end up costing you more money. Often, debt consolidation loans help you achieve a lower monthly payment and interest rate in exchange for extending the repayment period. If you stay in debt longer, you may end up paying more over the long term. Negative tax consequences. Depending on your financial condition, any money you save from debt relief services such as debt consolidation may be considered income by the IRS, which means you pay taxes on it. Credit card companies and other creditors may report settled debt to the IRS, which the IRS considers income. Bankruptcy is an alternative that eliminates your debt and gets you on the fast track to financial recovery. Call us at 636-724-3355 or visit at www.bankruptcysolo.com to take your first step to a fresh start. |

Brandee D. IannelliSt. Charles and St. Louis Bankruptcy Attorney Categories

All

St. Charles and St. Louis Missouri Bankruptcy Attorney |

RSS Feed

RSS Feed